What the Heck is Welfare?

What the Heck is Welfare?

The sum is greater than its parts

With it being the holidays, I thought we should talk about the basics of welfare economics.

I hope the refresher is helpful and allows us to avoid some confusion.

First, a bit of “background”: Bryan Caplan wrote a post on price discrimination, a favorite topic of mine. I’m a big fan of price discrimination, even if sometimes it hurts welfare.

An online discussion of Bryan’s post then led me to an old post by Nick Rowe, where he claims perfect price discrimination is actually inefficient in general equilibrium. I read Nick’s argument as follows:

If a producer sets its price equal to your willingness to pay, you get no surplus.

If all producers set their price equal to your willingness to pay, you get no surplus from consumption.

If you get no surplus from consumption, you have no incentive to work.

No work is obviously not efficient.

Since we have GE theorems that prove perfect price discrimination is efficient for a wide, standard class of economies, I thought it was worth digging a bit into the details more, so we can understand where the disagreement comes from.

In this post, I will first remind everyone of what welfare is and why welfare depends on the definition of the good you’re talking about. Then I’ll extend that analysis to multiple goods and see what changes. Then we will have the tools to go back to Rowe’s claim and see that his leap from 1 to 2 does not hold in general.

The Basics of Welfare Analysis

Let’s take a step back: what is welfare? It is important to remember all welfare analysis involves a comparison. It bakes in the economist’s favorite question: “compared to what?”

If we are being a little fast and loose, in “partial equilibrium”, welfare is a measure of gain because that particular market exists, or that trade is allowed. We are doing a counterfactual where the market is either eliminated because the price is too high or the government simply bans it or something like that. If we define the market differently, we get a different measure of welfare. In “general equilibrium,” welfare is a measure of gain from all markets existing. It is welfare compared to autarky, where all markets are shut down.

Throughout I will focus on consumer welfare/surplus. The same can extend to producer surplus.

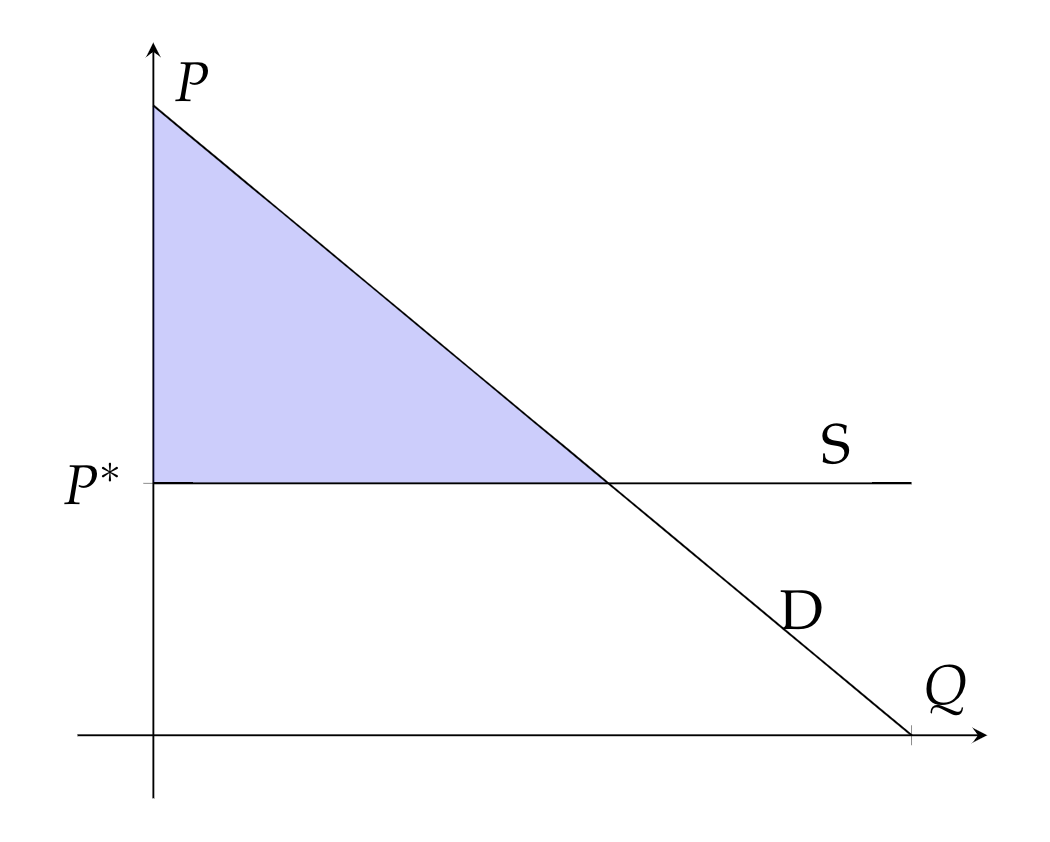

To calculate consumer welfare, we first calculate a demand curve, where the amount demanded is a function of all prices: x*(p). We can then plot the inverse demand curve D and calculate welfare for any market price P*; it is the area between the demand curve and the price, as the area shaded in blue. The total area can be thought of as the equilibrium gain versus a situation where the market is banned or where the sellers set the price above anyone’s willingness to pay.

Quick sidebar: Remember that a demand curve already builds in what is happening in the other markets. By construction, the demand curve takes into account that people will change their behavior in other markets as the price changes. For example, the demand curve builds in the cost of earning money. If the price were too high that you wouldn’t purchase any of the good, maybe you would work less. Maybe you would work more. That is already factored into your demand curve and your willingness to pay for the good and therefore into the calculated surplus, so contrary to Nick’s concern, that’s not really the issue. Any monopolist will implicitly take those changes into account because we assume the monopolist knows the demand curve.

Now back to the basics of welfare: it is important to be careful when we try to infer changes in welfare, since the welfare calculation already involves one comparison or difference calculation. You need to make sure you’re measuring against the same benchmark.

Let me show you how this can go awry.

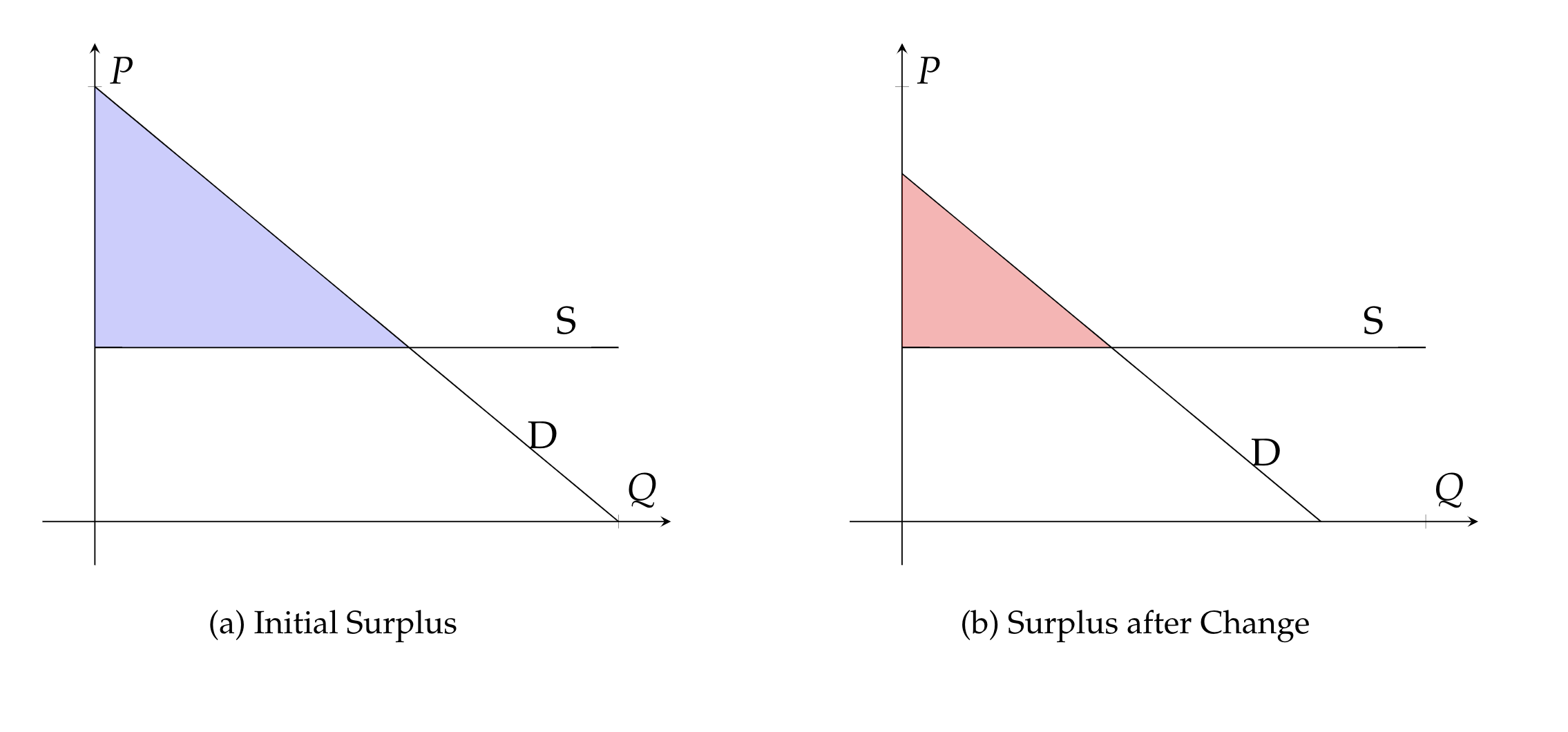

Take a standard partial equilibrium model. You calculate some consumer surplus as the shaded area. Start with an initial equilibrium on the left, where the consumer surplus is shaded in blue. Now suppose demand shifts in, as shown on the right. Consumer surplus in this market declines.

But we cannot conclude that overall consumer welfare declined!

We need to know more about the cause of the shift in demand before we can make any meaningful comparison of the left and right surpluses. If demand shifted in because the quality of this good dropped, then, yes, consumers are worse off.

What if the demand curve shifted in because the price of a substitute dropped? Obviously, overall consumer welfare increases if the price of goods drops, even if the welfare in this market is now lower.

The crucial difference is whether the reason for the change in demand is within the market we are looking at or whether it is outside. In partial equilibrium analysis, we can only make welfare comparisons if the change is to the market we are studying.

So we can still use partial equilibrium to compare the welfare effects of a tax on the good in the market we are studying👍. We can’t use partial equilibrium to compare the welfare change from another good’s price change 👎.

Welfare in Multiple Markets

The above issue highlights one of the key ideas in price theory: there is an interaction between markets and that interaction happens through prices. The role of the economist is to trace out the interaction.

In terms of welfare, the important implication is that welfare is more than just summing across markets; the sum of welfare across two markets is not the same thing as the total surplus.

Suppose there are two goods sold: gallons of milk and half gallons of milk. Now we ask, how much surplus is generated by the market for gallon jugs of milk? We then suppose that the market for gallon jugs was eliminated.

How much worse off would the consumers be without gallon jugs of milk? For the sake of this thought experiment, we can answer not very much, because, by definition of the market as the market for gallon jugs, everyone can still buy half-gallon jugs.

The same holds if we ask about the consumer welfare from the half-gallon jugs; it is pretty small. So we have that consumer welfare from gallon jugs is small and the consumer welfare from half-gallon jugs is small.

But we cannot conclude that the consumer welfare from milk is small. It is a completely different counterfactual; we are eliminating both markets. The most we can say in a standard model of substitutes is that the consumer welfare from all milk greater than or equal to the welfare of gallon jugs plus the welfare of half-gallon jugs.

For those interested in the technical details, read Makowski and Ostroy. The general theorem is that

total surplus >= sum of each market’s surplus.

Back to Price Discrimination

Now let’s return to price discrimination by multiple firms, or “general equilibrium” as Nick Rowe is considering. We can show that each firm capturing all of the possible consumer surplus from its product does not imply that all firms collect all of the possible consumer surplus.

Consider a case where there are two firms that produce two physically different goods. Consumers are price-takers and will only buy one unit between the two markets. But instead of the firm’s being price-takers, firms get to set their own price.

First, for simplicity, suppose the goods are so close that all consumers think of them as perfect substitutes.

Now, suppose the second firm is setting a price of $1 for its good.

What is firm 1’s residual demand curve? Since everyone can go to the other firm and buy a perfect substitute for $1, their willingness to pay for firm 1’s good is only $1.

If we only look at firm 1, we have a firm that is setting a price exactly equal to each consumers’ willingness to pay. They are perfectly price discriminating, even though they don’t need to actually set different prices.

Again, we cannot then infer that total consumer surplus is zero.

We can further complicate the model so that the goods are not perfect substitutes and so that each firm does face a downward-sloping residual demand curve. But that’s not really necessary.

The key is again total consumer welfare is not just the sum of consumer welfare, looking firm by firm at their residual demand curve. The reason is that one firm’s pricing affects the other firm’s residual demand curve.

The point is bigger than just welfare. Even though we often draw partial equilibrium curves, price theory is really about tracing out the interaction between markets. As Alex Salter once put it, price theory is general equilibrium reasoning using partial equilibrium models.