Take Supply and Demand Seriously, Not Literally

Take Supply and Demand Seriously, Not Literally

Market competition is more pervasive than just price and quantity

Welcome back to another installment of Economic Forces! I hope everyone is having as much fun as we are.

In my last newsletter, I explained some common mistakes people make when talking about competition; people often get the theorems wrong.

But here at Economic Forces, we are about using price theory as an engine of analysis, not theorem-proving. We want to use the theoretical tools to learn something about the world, not just solve for P and Q. Sometimes that means we need to move beyond the formal results.

Consider the following observation from Armen Alchian and Bill Allen’s textbook (I forget which version I found it in. Sorry.)

How do we know that demand curves are downward-sloping? Look at advertisements. Firms always advertise when their prices are lower. They never advertise higher prices.

I thought this was a nice insight from Alchian and Allen. As with everything they write, I am a sympathetic reader.

Here’s what I think Alchian and Allen are trying to get across: suppose customers believe the price could be $1, $2, or $3, with equal probability, so the expected price is $2. Since the expected price is $2, only those people who are willing to pay $2 or more will go to the store to buy the good. Since everyone that goes to the store is willing to pay $2, the business can set a price of $2. Fine.

But now suppose the business realizes that they didn’t sell as much as they expected. The business has “excess supply.” To sell the rest of their goods, they need to lower the price and get the people willing to pay $1 to come and buy their goods. To get people to come to the store, they advertise to customers that prices are lower.

If there was instead an excess of demand because the firm set the price “too low”, the firm would not need to get the word out. They would simply have customers that leave without the good. Next time, they may raise prices to resolve this problem, but they definitely do not need to advertise!

If that’s the way the world works, then we will see firms advertising when they only lower their price. Since I have set to see advertising for higher prices, I buy Alchian and Allen’s story and think that this is a nice illustration of the implications of the law of demand.

But notice, unlike my last newsletter on the formal properties of competitive markets, this is not actually a formal result. It’s not a theorem; we do not have a benchmark model of this process of price adjustments.

In fact, as people were quick to point out, the standard interpretation of supply and demand does not allow for such behavior. With supply and demand, prices do all the work to maximize profits and clear markets. So advertising and the law of demand are really orthogonal issues. If you take supply and demand literally and think that price is the only form of competition that would occur in a market, the logic makes sense.

So what the heck Alchian and Allen?

I want to convince you that this is not the right way to think about economic models. The literal interpretation would completely hamstring supply and demand as an engine of analysis.

And if we are going to take the models 100% literally, this does not just hamstring supply and demand. Advertising doesn’t show up in the monopoly model either! If the company had so much market power, why would they spend any money on advertising? Why wouldn’t they just raise prices to capture more surplus?

So can we just not talk about advertising? Instead of explaining things to a first-year student, we would need to trudge through years of more formal modeling before saying anything interesting.

That is a ridiculous way to use models. And I say that as a theorist (albeit a not very good one) who spends his research time taking models literally.

Before my fellow theorists hang me, I’m not arguing for an “anything goes” approach to economic theorizing.

We still need to take supply and demand seriously and work through the logical implications: what does it say, and what does it not say? My interpretation of Alchian and Allen gives an empirical implication. It does not say anything goes.

This shouldn’t be anything new for economists. We all explain to our 101 students that if the price is above the equilibrium price, the quantity demanded will be below the quantity supplied, so there will be suppliers left without a buyer. Those suppliers will have an incentive to lower their prices to sell their goods. This process pushes the price toward equilibrium.

Economists are rightly comfortable working through these dynamic arguments, even if supply and demand, taken literally, is a static model. I don’t lose sleep over teaching this to students without an explicit model to point them to. I hope you don’t either. (As a researcher, I do lose sleep over this and work hard to build dynamic models, but that’s different.)

On the margin, I urge economists to be more comfortable taking the models seriously but not literally. The new insights generated, when properly wielded, makes up for the lack of formalism.

Let me give one more example, shamelessly stolen from the Chicago Price Theory textbook.

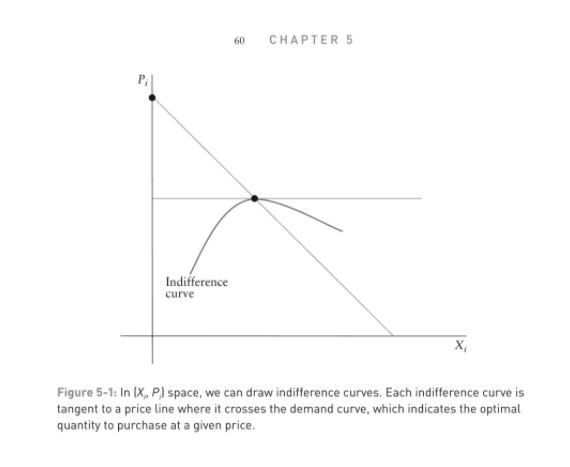

Consider someone’s demand curve, as given in the graph below. We can draw an indifference curve for that customer on the same graph. Consumers prefer lower prices, so utility increase as price decreases. At a specific price, given by the horizontal line, the highest indifference curve that the customer can reach price is at the black dot. Buying more or buying less makes her worse off.

If given the free choice of what quantity to buy at that price, the customer will choose the dot. That’s just a roundabout way of saying that is the quantity demanded at that price.

The literal interpretation of demand assumes that you are always exactly at the point. But that’s a little extreme. Don’t you think? What if we want to consider the possibility that, maybe, just maybe, you can’t buy the exact quantity specified by your demand curve.

Are we stuck saying nothing because the model doesn’t allow actually allow you to be off your demand curve? I think not.

Here’s where the indifference curves come in. Not all errors/failures to be on your demand curve are equal.

The curve shows how being a little off of your demand curve in terms of quantity does not really affect you. If you buy a bit more of the good than you truly want, say you want 9 oz but the can of beans only comes in 10 oz, you really don’t care. It’s not worth it to find a shop that sells 9 oz cans.

If the quantity does not really matter that much, what does? The indifference curves show that you really care about the price! If you overpay relative to another seller, that bites.

So now we can start thinking about what the implications of this idea are. I encourage all my readers to watch Kevin Murphy work through these implications. For me, the main takeaway is, again from Murphy,

I might shop real intensively on price and then when I get into the supermarket just throw crap in my cart.

That’s what I do. Go to Walmart because prices tend to be lower and then just throw crap in my cart. That’s what economics predicts!

For people interested in thinking more about this, in addition to Chicago Price Theory, I encourage you to check out McCloskey’s intermediate textbook as well, especially Chapter 12. She works through what happens when firms do not perfectly minimize costs, as the model assumes.

For example, even though all basic models assume cost-minimization (it’s actually tautological, who wouldn’t minimize costs?), we can still work through what happens if people do make errors. For example, errors are much more costly for a competitive firm (which may be driven out of the market for smaller errors) while not mattering that much more firms with market power. The selection mechanism is more intense in competitive markets.

I’m fine making that claim without an agreed-about evolutionary model that we all use. Save your theorem proving for another topic.